growing

like nuts

| |

|

||||||

|

growing

like nuts |

index | ||||||

|

|

|

|||||||||||||||||||||||||||||||||||||||

Summary according to VREG registrations*: Milestones March 2011: 100.000 PV-installations in Flanders surpassed. Biggest free-field PV-installation of Benelux included (2x 6,2 MWac Nyrstar project). Accumulated capacity up till December 31, 2010, according to latest month report revision (status: Apr. 5, 2011): 726,948 MWac with 96.609 registered "installations"**. Accumulated capacity up till latest month report, April 5, 2011: 747,294 MWac with 100.935 registered "installations"**. Market

growth January 1, 2011 up till April 5, 2011: Difference between latest Apr. 5, 2011, and previous Feb. 28, 2011 report: 3.575 registered entries with 50,567 MWac (app. 11,2 MWac extra attributed to 2009, app. 25,4 MWac extra to 2010). Accumulated capacity end of 2009 (VREG update/review April 5, 2011***): 534,895 MWac with 65.248 registered entries (average size all installations: 8,20 kWac/entry). Preliminary market growth for 2009 - based on new numbers published by VREG, Feb. 28, 2011 (dramatically increased with respect to 2009 year report published May 2010), and continuously revised in later reports (status: Apr. 5, 2011): 442,059 MWac with 49.897 "installations" (average size new installations 2009: 8,86 kWac/entry). Preliminary, calculated market growth for 2010 (Jan. 1, 2010 up till Jan. 1, 2011): 192,053 MWac with 31.361 registered entries (average size new installations 2010: 6,12 kWac/entry). Total growth in period 2009-2010: 634,112 MWac with 81.258 registered entries (further increase expected with backlog being registered in future VREG reports). Serious downfall of newly added registrations in January 2011 for >10 kWac category: only 8 (1,418 MWac new). In February 28, 2011 report "revival" with 54 new in this category (9,490 MWac), in April 5, 2011 report 115 were added (33,391 MWac). Installations with a capacity of max. 10 kWac registered by VREG make up 58,5% of the (documented) Flemish PV-market and have an average size of 4,40 kWac. 1.589 installations registered with VREG have an inverter capacity > 10 kWac. The biggest "single-site" installation is the multi-roof Loghidden City terminal of Katoen Natie (Schelde West Bank) with at least 27,51 MWac inverter capacity. Heusden-Zolder 4,704 MWac Zonnecentrale Limburg NV, for a long time the largest free-field installation registered as such by VREG, has been replaced by 2 preliminary large entries for Zonnecentrale Overpelt NV in the April 5, 2011 report. These entries probably represent a solar parc over 12,4 MWac in size. By far the largest in the Benelux. * Note that a considerable volume of registrations in 2009 seems to have been attributed to a large contingent of installations at the end of 2009 with the modules already fixed in place, but that were given time up till end of February 2010 to have inverters installed and a certified installation connected to the grid (these installations all get 45 eurocents/kWh for the green certificates, all other grid-connected PV-systems in 2010 "only" 35 eurocents/kWh). If one would take "grid connection of a complete installation" as the decisive point in time, these PV-systems were "formally delivered" in 2010, not in 2009. Apparently VREG decided otherwise, or regulations were not clear on this important point. The "choice" to allocate such a large volume to either the former or the later year has, of course, huge impact on "officially newly installed" capacity in a certain year, such as incorporated in national (Belgium) and international (e.g., EurObserv'ER, EPIA, etc.) statistics. ** Certified, registered with VREG, and prone to receive green certificates for the electricity produced. Note, that many several larger PV-systems are not reported "as one system", but as two or more separate entries in the VREG registrations. The biggest "multi-roof" installation on one site, the huge Loghidden City Complex on the western Schelde shore (Kallo Kieldrecht), and part of the 40 MW Katoen Natie super project, has been split into at least 22 separate parts (varying in size between 210 and 1.804 kWac in the VREG reports) filed under the name of several daughter companies of the Katoen Natie holding (status: Apr. 5, 2011). Similar split-ups appear in the Desteldonk area of Gent for the Katoen Natie project, and are frequently encountered with a variety of other bigger installations of hundreds of kWac. In the VREG reports, the "entries" are referred to in Dutch as "productie-installaties" (installations for production of renewable electricity deemed worthy of receiving guarantees of origin). *** Still not definitive numbers, data can - in particular for most recent years will - change in coming year report(s). |

Results from the market statistics produced by the "Vlaamse Reguleringsinstantie voor de Elektriciteits- en Gasmarkt" (VREG) for PV market development in Flanders. Statistics are frequently refreshed on VREG's website, but sometimes lagged behind 1-2 months due to serious work overload at the regulator's office (since April 2010 there has been, however, a continuous update per month). It must be emphasized here that older "numbers" reported by VREG can still be updated afterwards, as can be found in the [updated] year reports by the regulatory authority, and also, since 2011, in extensive, updated month reports. Hence: earlier published year accumulation for PV-capacity, can be changed as a backlog of installations not yet covered for that year is added even years later. This was particularly so for the data for 2009, that VREG first revised officially in their Feb. 28, 2011 month report (dramatically increasing capacity and installation numbers for 2009 compared to the 2009 year report). This realisation made Polder PV update his earlier data on basis of VREG's yearly reports, and update his graphs published sofar. Updates will be further provided with each month report.

Graphs made by Polder PV from the principal VREG data (and other sources) are found directly below (roll-over image). Data for earlier years (up to 2004 from graph published by ODE, this webpage) have been replaced by new VREG data published in the Feb. 28, 2011 report. The latter report is now the first reference for new analysis, which will be augmented by new data in monthly reports as of March 2011. Note: data in these graphs are only for the "Vlaamse Gewest", the Flanders territory excluding Brussels, and also not including the large French speaking Walloon region. See the separate sections for these areas on this page. These data for the much smaller Belgium markets still have to be updated. An analysis with most recent data (but with the older, "then latest available" VREG data for Flanders) has been published by Polder PV in an article published for the 2010 Solar Future Belgium symposium by SolarPlaza (original article here).

MWac, not

MWp

Note

that data published for the Belgium market appear to relate to maximum

inverter capacity

involved (kWac), and do not refer to nominal STC power of the DC generator

(kWp), as previously thought. Polder PV, on asking VREG, what accumulated

MWp power could be on Flemish soil, got the reply that this is unknown

for many older installations, and that such data have not yet been compiled

by the regulator. A "standard calculation factor" to obtain MWp

power from the registered MWac data is not used by VREG because of the

uncertainties

therein (e-mail

reply March 8, 2011). If one would calculate in a conservative manner,

one could multiply the AC power in the tables and graphs with a DC generator:AC

inverter capacity factor 1,1 (hence: on April 5, 2011, Flanders could

have accumulated 747 (MWac)

* 1,1 = 822 MWp of nominal DC power (STC capacity of PV-modules involved).

This remains, however, an uncertain value as long as VREG is unable to

provide more details.

For population data (mid 2010), the number of inhabitants for the Vlaamse Gewest only has been taken ("Vlaamse Gewest" app. 6,3 million, "Vlaamse Gemeenschap" including Brussels would have app. 7,2 million Flemish inhabitants, according to this Wikipedia site). Data for Flanders are compared with data available for the Netherlands in the graphs. For further information please contact the webmaster of Polder PV.

Total

market growth for Flanders in 2009

New calculations had to be done based on the new

data published by VREG in their February 2011 report and later

revisions. Originally, VREG, published a volume of 245,051 MWac

and 47.273 new installations

for 2009, in their year

report for that year (dated May 2010). This has been grossly adjusted

in the new data. This is probably the result of the fact

that many installations have been mounted end of December

2009 without inverters, for which two months extra time in 2010 was

given by the Flemish authorities ("transition period").

This to the effect of finalizing the installations and be able to

apply for the "old"

45 Eurocents per kWh (green certificates value), instead of the 35

Eurocents that was valid for all other new installations as of Jan.

1, 2010 (up till the end of that year). Possibly VREG originally

counted

(part of) those installations finalized before end

of February

2010

as belonging to the "2009 cohort".

The latest VREG numbers in the Apr. 5, 2011 year market update are: 49.897 new installations in 2009 (5,6% over the year report 2009 value), and a respectable 442,059 MWac of new capacity (80,4% over the previously reported volume in the first year report...). That is roughly a factor 74 as much as the absolute "growth" in DC power for PV (2009, data CertiQ) for "certified PV-installations" [app. 6 MWp], and 41 times as much as the total new capacity sold in 2009 (10,7 MWp) according to the most recent CBS statistics in the Netherlands bordering Flanders in the north.

Previous

estimates

In

an article in February 2010, Photon International claimed a capacity

of 275

MWp (DC generator capacity) for the whole of

Belgium in 2009

[PI issue 2-2010], which appeared to be highly underrated since

the Walloon region and Brussels should be counted on top of the

VREG adjusted

431

MWac for

Flanders only. In

another article, published by the German Photon equivalent in

the September

2010 issue (see also electronic

version), it was suggested, based

on sources with the Flanders branch organisation BelPV, that

a

new

capacity of 301,8 MWac could have been added in

2009.

And that in the whole of Belgium 345,2 MWac

would have been newly built in that year. In

a short message in the first Photon magazine of 2011 (January issue,

p. 13), mentioning "only

105 MW growth" for

2010 (most probably AC power), they referred to VREG and stated that

it might have been even "four

times more" in 2009, suggesting a volume of app. 420 MWac for

that year.

Finally, in a short article published on December 30, 2010, on the Dutch website Energeia, a Belgium reporter, Koen Mortelmans, cited BelPV with new numbers for Flanders in 2009: 412 MW (most probably AC power), also citing that in the first 11 months of the following year 2010 "only 100 MW" would have been added, while a small end-of-year-rush could result in an extra 80 MW (hence: expectation of only 180 MW new capacity in Flanders for 2010 by BelPV). These volumes had been re-adjusted to 412,7 MWac for 2009, and 165,0 MWac for 2010 in a graph in the "Marktcijfers PV" overview by BelPV (February 2011).

All these estimates - that now all appeared to be on the (very) low side - show that it remains difficult to obtain a reliable picture of ultimate market realisation, and that in the end market growth in Flanders seems to have been bigger than expected even by well-known PV-market analysts. With the important notice that VREG still can adjust their latest data, like they have done in previous year, and now also monthly reports. These adjustments always were in a positive direction: more installed capacity than previously published.

In the graphs presented below I will first give the latest year results (or: predictions) up till 2010 from the most important sources for the Flemish market: regulator VREG and branche organisation BelPV. All graphs give AC power of installations (note: deviating from common practice in Germany, where DC power capacities are published, "Generator Leistung" in kWac, MWp, etc.).

|

ROLL-OVER IMAGE. Mouse pointer away from the image shows the most recent available data from VREG (revised year data renewable electricity generation capacity as of Apr. 5, 2011). Mouse pointer over the image shows the previous data from year report 2009 and monthly updates up till Jan. 2011. For 2009/2010, changes are remarkable. Apparently the "end of year rush" installations in that year, that were officially allowed being certified as "connected tot the grid" as late as end of February 2010, have now been allocated to the year 2009 (instead to 2010). Hence, the 2009 year report capacity data will probably be revised as such in the coming 2010 year report. Note that capacity is in AC power (maximum inverter power of the installations involved). Total installed nominal generator power (MWp STC tested power of all PV-modules) is as of yet unknown for many older installations by market regulator VREG, but could conservatively be taken as 1,1 times AC power. |

Yearly added new PV-capacity (grid-connected) in Flanders completely revised by VREG, in their February 28, 2011 month report (mouse pointer away from graph). The changes with respect to previous known numbers (mouse pointer over the image) are staggering for the year 2009: Following data from the year report 2009, VREG originally published preliminary new capacity of 245,1 MWac for 2009. This has been changed into a considerable higher 430,8 MWac in the Feb. 2011 update (76% more capacity than previously published). In the April 5, 2011 report (not shown here), it was further extended to 442,1 MWac. The originally calculated new capacity for 2010, 320,1 MWac, followed from the monthly reports published in 2010, but had to be revised accordingly: the preliminary new capacity for that year in the April 5, 2011 report appears to have been only 192,1 MWac, 40% less. This probably is the result of a re-allocation of the end of year 2009 installation numbers "as having been grid-connected in the year 2009 instead of in the year 2010".

Branche organisation BelPV implied 412,7 MWac for 2009 (smooth green column) in a graph published in February 2011, and a preliminary 165 MWac for 2010. End of 2010 they predicted a small "end-of-year-rush" of possibly 80 MWac in December 2010, that apparently has not materialized in the VREG data published sofar (or it did not happen tot the extent that was anticipated). The strange thing is, that Jo Neyens of BelPV has been one of the 2.943 people, organisations and companies (status: Jan. 20, 2011) signing the petition to the Flemish government ("Laat de zon schijnen" - "Let the sun shine") to prevent harsh degression measures for the coming feed-in tariffs for PV. In that well-written document, dated November 25, 2010 (one of the authors works for the well-known PV-system planner Enfinity), the old market data by VREG (that I originally took as a basic reference) were also used for the calculations (pages 7-8 of the pdf available through that website). There they also took the VREG year report 2009 data, and the following month reports as "true market data" to calculate the probable volume of kWh's produced (and green certificates to be issued) based on that market growth.

If the resulting end of year "accumulation" of installed capacity is calculated from the given (new) data by VREG and BelPV, or derived from the data in the last month reports for 2011 by VREG, the following picture emerges:

In this graph end of year (up till 2010) accumulations have been shown following from the predicted (or, in the case of VREG: newly published) yearly growth rates. The outcomes for the updated VREG registrations and those derived from BelPV's "yearly market growth numbers" now lie close together (there used to be a huge difference). In addition, with the first three month reports by VREG for 2011, and the revisions therein, accumulation of all registered installations already has become 747,294 MWac. If one would take 1,1 as a conservative multiplying factor to calculate the possible DC generator power involved, this could amount to approximately 822 MWp (STC power of all PV-modules).

2010

onwards - overview and details

The

market segment > 10 kWac (status April 5,

2011) could be analysed in detail. For the first time, in the January

31, 2011 issue, the long installation list (pdf of January 1, 2011

report containing 140 pages)

was

published as an Excel file. After reworking that file, it was

much easier to compare that listing with the previous one and extract

from the differences the growth data in the intermittent period.

Regrettably, later reports again were pdf files, so that all pages

had to be screened meticulously to check for changes.

From the first report for 2011 it immediately became clear, that there has been low growth in new registrations for >10 kWac installations in the January 2011 report, for details see graphs showing all month data. In February 2011 the trend has been strongly upwards again, further strengthened in March 2011. In the April 5, 2011 report, VREG-registered PV capacity in this specific category consists of 1.589 installations with an accumulation of 310,3 MWac of inverter power, and an average system (or "entry") size of over 195 kWac.

Small system

size/accumulation

Taking

the accumulation of installations >10 kWac counted by me (and included

in detailed spreadsheets), and subtracting that volume from the separate "accumulation

for all renewable

options"

listing

by VREG, it is possible to calculate the share of the installations

up till 10 kWac ("small market segment"). On April

5, 2011, that segment seems to represent

(calculation here)

an accumulation of 99.346 installations with 436,981

MWac of installed

capacity and an average system size of 4,40 kWac (calculating

with a factor kWac = kWac * 1,1, average STC generator (DC) size for

this important category could be over 4,8 kWac).

Growth numbers

PV-categories big and small

Additions

of new registrations in the last months has been relatively modest

according to the VREG

administration,

in general showing a slacking off the pace shown in 2009. Sofar, the

January 31, 2011 report was a "record breaker" in that negative

trend, with only 8 new additions for installations > 10 kWac, and 2.942

for the "small" category

up till 10 kWac. That negative trend has been reversed in the February,

2011 report, with the important annotation that many new entries are for

previous years, even including installations officially declared installed

in 2009. Reporting from the results from the last months

("installation" meaning:

"entry registered in the VREG records"):

September 2010 (between Sep. 2 and Oct. 1): 91 installations > 10 kWac with 24,07 MWac (average size of 265 kWac/installation) added (note: incl. new additions for previous years). Growth for the market segment up till 10 kWac has been 3.572 new installations with a size of 16,98 MWac (average size app. 4,75 kWac/installation). Total "VREG-registered" additions in 30 days (Sep. 1 up till Sep. 30) has been 41,05 MWac and 3.663 new installations, or 1,37 MWac (122 installations) a day. October 2010 (between Oct. 2 and Oct. 28): 34 installations > 10 kWac with 12,26 MWac (average size of 360 kWac/installation) added. Growth for the market segment up till 10 kWac has been 2.208 new installations with a size of 10,41 MWac (average size app. 4,71 kWac/installation). Total "VREG-registered" additions in 28 days (Oct. 1 up till Oct. 28) has been 22,62 MWac and 2.242 new installations, or 0,81 MWac (80 installations) a day. November 2010 (between Oct. 29 and Dec. 1): 61 installations > 10 kWac with 10,65 MWac (average size of 175 kWac/installation) added. Growth for the market segment up till 10 kWac has been 3.098 new installations with a size of 14,79 MWac (average size app. 4,77 kWac/installation). Total "VREG-registered" additions in 34 days (Oct. 29 up till Dec. 1) has been 25,44 MWac and 3.159 new installations, or 0,75 MWac (93 installations) a day. December 2010 (between Dec. 2, 2010 and Jan. 1, 2011): 47 installations > 10 kWac with 10,53 MWac (average size of 224 kWac/installation) added. Growth for the market segment up till 10 kWac has been 5.181 new installations with a size of 25,28 MWac (average size app. 4,88 kWac/installation). Total "VREG-registered" additions in 31 days (Dec. 2 up till Jan. 1) has been 35,81 MWac and 5.228 new installations, or 1,16 MWac (169 installations) a day. January 2011 (between Jan. 2, 2011 and Jan. 31, 2011): only 8 (!) installations > 10 kWac with 1,42 MWac (average size of 177 kWac/installation) added. Growth for the market segment up till 10 kWac has been 2.942 new installations with a size of 14,47 MWac (average size app. 4,92 kWac/installation). Total "VREG-registered" additions in 30 days has been only 15,89 MWac and 2.950 new installations, or 0,53 MWac (98 installations) a day. February 2011 (between Feb. 1, 2011 and Feb. 28, 2011): 54 new installations > 10 kWac with 9,71 MWac (average size of 180 kWac/installation) added. Growth for the market segment up till 10 kWac has been a healthy 3.594 new installations with a size of 16,78 MWac (average size app. 4,67 kWac/installation). Total "VREG-registered" additions in 28 days has been 26,48 MWac and 3.648 new installations, or 0,95 MWac (130 installations) a day. March 2011 (between Mar. 1, 2011 and Apr. 5, 2011): 104 new installations > 10 kWac with 29,56 MWac (average size of 284 kWac/installation) added. Growth for the market segment up till 10 kWac has been 3.471 new installations with a size of 21,01 MWac (average size app. 6,05 kWac/installation). Total "VREG-registered" additions in 36 days accounted to 50,57 MWac and 3.575 new installations, or 1,40 MWac (99 installations) a day. |

From the above-mentioned data, it has become clear that growth rate in Flanders has slackened in 2010-2011, although growth rates still remain much bigger than in the neighbouring Netherlands (realizing only 11 MWp DC capacity of certified installations in 2010, and an unknown number of uncertified systems).

Market growth

2010

In the April 5,

2011 report adjusted preliminary market growth data for 2010 have been

published by VREG. 192,053

MWac of

new capacity with 31.361 new installations (average new system size:

6,1 kWac). See also the graphs published above. That new, preliminary

"official" volume is 57% below the new capacity

for

2009 according to the last published, official VREG data (growth

for 2009 according to latest VREG data: 442,059 MWac).

It is to be expected that this slackening trend will continue, in particular as rapid downward adjustments of green certificate values for PV has been - finally - agreed upon by the Flanders government for coming years (see interactive graph in this article). Much will depend on the system prices in the market. If these drop considerably, "good growth" still is a possibility for smaller installations. Perspectives for large, industrial size PV-systems, seem to be dire, as reported by branche representatives, in their "appeal" to the government. There is, however, still a large backlog in installations that could become visible in the VREG records in coming months, since an article in Energeia (dated January 21, 2011) showed a considerable number of requests for large installations reported by VREG, with a peak in March (over 120 requests), and another in December (117 requests). Many of those "high-impact" installations still can see the light in coming VREG reports.

Market growth

2011

Since the Feb. 28, 2011 report interesting new data have become available.

One of these is the "adjusted" volume listing per year (since 1985),

with the latest available data for the number of PV-installations

newly

installed

in the year under consideration. And considered eligible for receiving

green certificates by VREG. The original year of installation is

the marker date. Later expansions of installations, a practice common

with a growing number of PV-owners with appetite for more, are considered

separately. If that expansion has an official installation date in

a later year, it is assigned to that year.

For the first two listings (Feb. 28 and Apr. 5, 2011), I constructed this Excel table in which the "backlog" assignment per year can be followed in detail, for number of installations as well as their accumulated new capacity:

(Graph/table

above)

In this screendump of another spreadsheet a comparison is made between

the listings of PV-installations assigned to their (first) year of

installation as approved by VREG in two subsequent month reports (Feb.

28 and Apr. 5, 2011, respectively). In red numbers, changes in the

April report are given with respect to the data provided in the February

report. Sometimes even negative numbers result from that subtraction

(e.g., for PV-capacity changes in 1999 and 2007), possibly referring

to

removed

or destroyed

installations.

However, the most significant changes are positive, and dramatic for the last three years (2008-2010), with changes of 11,2 (2008), 25,4 (2009) and 13,4 MWac (2010) increasing the "new capacities" for those years with fairly big volumes (plus 0,7%, 2,6%, and even 15,2% for 2010). Hence: "actual" market growth data for Flanders and many other regions always should be considered with prudence.

From these two reports follow that in total 50,6 MWac of "accumulated PV-capacity" has been added in the latest, April 5, 2011, report, with 3.575 new installations. But that "only" 13,4 MWac (2.798 installations) has been added to the volume for the present year 2011 with this report, and the rest has been assigned to previous years. Still, many more installations can be added afterwards, to 2011 as well as to the years before. So it is to be expected that the 2011 growth will turn out to become much stronger than shown in the present update: up till the April 5, 2011 report an accumulated new capacity of 20,3 MWac. This "preliminary" volume for the first three months of 2011 is almost twice that of the accumulated certified new installations in the twelve months of 2010 in the Netherlands (with a population 2,6 times smaller in Flanders). With more capacity to be added on the horizon.

Graphs Flanders PV market as compared with Netherlands.

With the January 1, 2011 report, it has turned out that the VREG registrations have resulted in a historical "marker" event: Flanders surpassed the ("official") 100 Wac/inhabitant accumulated installation milestone in that report (with later revisions bringing more capacity for earlier years that marker shifts to a point earlier in time). On April 5 2011, with 747,3 MWac of registered capacity, the 6,3 million inhabitants of Flanders each had 119 Wac virtually installed inverter capacity. Using a factor 1,1, this could result in a virtual, average 130 Wp PV-module on the roof of each inhabitant, such as evident from the interactive figure given below. In this figure also the deplorable situation in the Netherlands becomes evident (green columns), with only something between 4 and 5 Wp/inhabitant at the end of 2010 (just slightly higher if the uncertified new capacity for 2010 becomes known, possibly in the spring of 2011 or later).

It is important to emphasize that Flanders has started only seriously in 2006 with market expansion as the first feed-in legislation was introduced in that year. Netherlands already has considerable experience in PV-installation since the end of the nineties of the previous century, but stifling political desinterest, powerful bureaucrats with their own "visions" of the energy future, and continuous sabotage by parties deeply involved in fossil-based energy generation has prevented succesful implementation of "working" legislation.

The following graph is updated with the data from the April 5, 2011 report. Note that older numbers will have changed, since a backlog of entries still is added on a monthly basis. The numbers give the extrapolated MWp nominal capacity (factor: MWp = MWac * 1,1) based on the published month reports by VREG:

ROLL-OVER IMAGE (above).

Moving the mouse pointer away from the image shows the absolute grid-connected PV

capacity accumulation as provided in monthly reports (note: most

recent data can change afterwards). Given directly in MWp by CertiQ

in Netherlands, but calculated by Polder PV from the AC power registrations

by

VREG for Flanders by multiplying those data with a factor 1,1*.

All installations certified for Flanders, but only a small, app.

10% portion certified for the Netherlands, with status end of 2009

(CBS, all installations) and (columns with dashed outline) for

June 2010-March 2011 only the addition with certified new installations

in 2010-2011 known by CertiQ at the time of publication that the

month report was published.

Moving the mouse pointer over the image gives the calculated capacity accumulation per inhabitant ("per capita"). Both images show strong growth of the Flanders market as compared to the extremely sluggish development in the Netherlands - even under a new "incentive" regime. Calculated accumulated grid-connected capacity for Flanders April 5, 2011: 822 MWp of nominal (STC) capacity (747 MWp accumulated AC power). Ten and a half times as much as was probably accumulated end of March 2011 in the Netherlands (exclusive of yet unknown non-certified installations, see below). As of March 2009 I included the data published by VREG on an irregular, sometimes bimonthly basis.

December 2009 capacity accumulation for the Netherlands is based on the definitive 2009 year report published by CBS in August 2010). Actual accumulation of all installations (certified and, the largest portion, uncertified) is not certain. Grey imports are not accounted for, problems with inventarisation might be expected in a chaotic market, with many system providers not being member of branch organisation Holland Solar and possibly not included in the CBS statistics. Thus, true market growth could deviate in the order of several MWp. According to CertiQ month reports for 2010 data, possibly 2,3 MWp might have been added in the first month of 2010, but there is much confusion about the Dutch data, and CertiQ strangely reported two months of "negative growth" of certified installation capacity (possibly misreported installations, or systems that have been withdrawn from the CertiQ pool for unknown reasons).

According to the end of December 2010 CertiQ report, almost 11 MWp should have been registered as new, certified installations in the Netherlands, as of Jan. 1, 2010 (these should be attributed to the "SDE incentive regime" for installations with approvals in 2008-2010). This, added to the 62,5 MWp accumulation (grid-connected) end of 2009, gives a preliminary status of less than 73,5 MWp end of 2010. With extra additions of almost 3,8 MWp in following January up till March, total "known" market volume adds up to some 77,2 MWp, end of March 2011. The uncertified, not centrally-registered volume added in 2010 is as yet completely unknown (this volume, if registered in a representative manner by CBS, could have been approximately 40% of total capacity sold to end-users in 2009).

Comparison of market development of grid-connected PV-installations in Flanders (blue) versus the Netherlands (light green) is shown in the graph. The new "incentive" regime in the Netherlands (SDE, started on April 1 2008, in essence a combination of net metering [poorly documented in Law since July 2004] and a variable feed-in allowance changing each year) is so bureaucratic and full of various restrictive market caps, that progressive, strong growth has remained an illusion. From renewed calculations of published graphs (new calculations published here) only app. 6,7 MWp had been included as new certified installations in 2009 according to CertiQ data (possibly some lagging installation validations still to be added).

A growing number of system buyers did not even apply for the new SDE subsidies in the Netherlands because of stifling bureaucracy, and many uncertainties. Still, an increasing number of people and companies have acquired uncertified, mostly unreported PV-systems and still do so in increasing numbers. In their year report for 2009, CBS published data resulting in approximately 10,7 MWp of capacity sold to installers in 2009, 10,6 of which would be grid-connected. That indicates that app. 37% of capacity sold did not enter the CertiQ database, do not have a certified meter, and that its green electricity production is probably not registered in any central register. The new conservative, nuclear fission loving minister for economic affairs in the Netherlands, Verhagen, dictated end of November that in 2011 all state-induced incentives for "small-scale" photovoltaics (up till 15 kWac) would be completely abandoned, and that the economic basis for incentives for larger installations would turn out to make that a negative business case in the majority of projects... A plethora of - often short-lived - new "initiatives" has emerged since then. The national PV-market is in total chaos, and an initiative for buying cheap Chinese modules and inverters (app. 13-14 MWp) by a foundation (Urgenda/Wijwillenzon.nl initiative 2010-2011) has met with strong criticism by - mostly experienced - installers, fearing their hard-earned market shares out-competed with heavily subsidized Chinese hardware dumped on the ever-small Dutch market...

In

contrast

Flanders

has introduced an exceptionally attractive package of "Germany-like" (but

not identical) kWh incentive for 20 years (up till 2009 45 eurocent/kWh,

fixed tariff for existing installations, lowered to 35 eurocents/kWh

in 2010, and to a still acceptable level of 33 eurocent/kWh up till

April 1, 2011, with further strong reductions already decided

upon). Added with accompanying net-metering up till zero on a yearly

basis for the smaller installations (max. 10 kW inverter output), and

very interesting tax incentive measures. The Flanders market started

to grow like nuts in 2008-2009, as revealed by updates by VREG, showed

slower growth in 2010, and will probably slacken off to a lower level

as the market value of solar electricity will erode because of the

strong, step-wise degressions of the value of green certificates. In 2011,

"social cost" discussions (hotly contested by branch organisation

BelPV) have eroded political will to further support photovoltaics

forcefully. The social

Minister

Vandenbossche

has openly

"admitted" that PV has grown to fast, and she has pleaded

for more windpower in Flanders.

"Vlaanderen is een 'energetisch ontwikkelingsgebied'". Willy Lievens van educatief centrum Zonne-arc, in een artikel over zijn initiatief in Duurzame Energie van augustus 2001, en aanhanger van de Trias Energetica (besparen boven alles), zal mogelijk zijn mening daarover enigzins hebben bijgesteld anno 2011... |

Flanders: PV has most capacity installed in renewable electricity

© Data VREG, April 5, 2011 report

(Graph

above)

Already

in the end of November 2009 report by VREG, solar electricity had

reached the largest nominal electrical capacity of all considered renewable

options in Flanders,

and increased considerably up till the end of March 2011. Output

in kWh, of course, is much lower in relation to other renewable options

because of the relative low specific production per kWac (PV installations

are unable to produce anything at night). However, this graph shows

how

large the impact on the "renewable electricity market" has

become with respect to photovoltaics in this relatively small, Dutch-speaking

part of Belgium. A sizeable 44,6% of total "nominal" capacity

(1,674 GWe) installed is the most democratic type of electricity generation, "power

to the people" PV.

Renewable electricity generation from wind on land (blue column), which temporarily took over the second place in July 2010 with the installation of 4 new turbines (and 2 new ones in August of that year), has fallen back on an almost equal basis with the burning of biomass originating from agriculture or forestry, and occupied a 3rd position in the April 5, 2011 report according to the VREG data. It is expected that, with the building of an off-shore wind parc (and increased political support for wind on land over solar by Flemish authorities), this situation could change dramatically in the near future. There is, however, also a highly controversial old coal-plant that is refurbished by co-owner Electrabel as a pure "biomass-firing" plant fed with imported Canadian wood chips. This company, having a rather bl(e)a(c)k reputation in Belgium, and de facto a French-backed monopolist (under the umbrella of GDF-Suez), will obtain huge amounts of feed-in incentives extracted from the purses of all Flemish people (end of January also including 4,4 MWp in 15 PV-projects). A move that has loosened the tongues of many people there (Polder PV reported on November 26, 2010, and on December 11, 2010)...

Flanders: distribution among PV-installations > 10 kWac

One of the most interesting sections in the statistics reports by VREG is a detailed overview of the individual installations for the production of renewable electricity (for which green certificates are issued). Up till end of 2010, these data were published as - mostly - monthly pdf documents with a full list of all the installations. This list does not include the small (most PV) installations up till 10 kWac, but gives a fascinating overview of spread in installation size and companies involved, as well as their location (community with zip code). End of January 2011 for the first time this list was presented as an Excel file, facilitating update work. Regrettably, the publication format returned to pdf afterwards, seriously hampering quick analysis of changes between reports published.

Polder PV analysed the last March 2011 report (with 1.589 entries) in detail, extracted the relevant data for PV installations, and summarized the findings in detailed graphs below*. Update >10 kWac listing: April 5, 2011.

* Since data prior to 2011 have been - carefully - extracted from pdf documents, minor errors might have been included in the spreadsheets constructed by Polder PV. They will, however, have little effect on the evident trends published in the graphs published below.

(a) Accumulation of > 10 kWac installation capacity and numbers

2011 - a new year

Accumulation of number of registrations and of total capacity of PV-installations (MWac) up till the last VREG report, April 5, 2011:

|

© Data:

VREG; Graph: © Peter

J. Segaar/Polder PV, Leiden

(NL) |

Adjusted

numbers exlusive of Loghidden City

In

the April 5, 2011 again two new sections for the Katoen Natie

project have been registered in the VREG data (see special for

details about that project, the 2 new entries are both in the "Desteldonk"-named

part of the sea harbour region north of Gent). Average size for the > 10

kWac category has been 195,3 kWac per installation for all accumulated

entries recorded by VREG.

The following

basic data for the >10 kWac category exclusive of

the single-site Katoen Natie Loghidden City logistics complex in the

western harbour area outside of Antwerp (>27,5 MWac) could be extracted

from the April 5, 2011 update: 1.567 installations (or: separately

registered portions of large installations) with a total of 282,8

MWac

and

an average system size of 180,5 kWac per installation.

Big Players

and large installations registered

On top of Katoen

Natie

sub-projects discussed further below, several other big projects

are included in the VREG lists.

The September 1, 2010, update by VREG first added chunks of the Balta roof project in Wielsbeke by project developer Belfuture, the largest one being 2 MWac (Balta Group published a report on August 19, 2010, claiming a spectacular total of 11,5 MWp [DC capacity] of large PV-projects on 3 of its industrial sites). In a small revision in the October 28 update, three entries were reported as part of this specific project. Together they amounted to one of the largest roof installations (besides Katoen Natie) in Belgium: 4,2 MWp (DC capacity mentioned by Balta). The three entries add up to 4 MWac in the VREG reports. Hence, a DC/AC ratio of 1,05.

Three more > 1 MWac projects were registered in the October 1 report by VREG, one 1,04 MWac installation by Noordkaai NV on the Antwerp (east) side of the Schelde river bank, a 1,105 MWac project in Mechelen by Invictus Mechelen N.V. (the same company that engineered the Katoen Natie project), and a 1,59 MWac installation by SunCop I N.V. in Hingene southwest of Antwerp. Apart from 4 further Katoen Natie fragments > 1 MWac no other such big installations were reported in the October 28 update. The December 1, 2010 update reported another 1,728 MWac chunk of the Katoen Natie project, and a 1,68 MWac installation by Soless on the premises of AGFA in Wilrijk. In the January 1, 2011 report, a 1,012 MWac project bij Stas BV in Sint-Truiden was registered, and three portions of the Katoen Natie project in the Sint-Kruis-Winkel area bordering Desteldonk in the Gent sea terminal region (total of these 3: 4,755 MWac).

No further big (sub)projects appeared in the January 31, 2011 update. However, again two new projects emerged in the February 28, 2011 update. A 1,05 MWac project by Vergalle NV in the village famous for its Spring cycling classic (Ronde van Vlaanderen), Oudenaarde. And a new Seaport Terminals N.V. installation of 1,485 MWac on three warehouses at Mai Zetterlingstraat 70 in Desteldonk. Strangely, that is the same address as a previous entry of the same size under the same company name, with the same zip code, but allocated to Sint-Kruis-Winkel, at the same location just northeast of the Gent harbour region. On that same address 3 other entries of huge installations sized 1,1-2,2 MWac under daughter companies from Katoen Natie (Polymer NV, Sabeen NV) have been included by VREG (however, on other warehouses at this address). It is not yet clear if the "Seaport Terminals N.V." entries actually belong to the famous Katoen Natie project, or that it really is a separate company having done the same thing as their neighbours once they saw how lucrative the solar megabusiness was.

The April 5, 2011 report saw 2 new Katoen Natie entries in the Desteldonk region of Gent (3,11 MWac), and 2 new installations by Invictus, one in Niel (Invictus Boom, 1,084 MWac), and one in Puurs (Invictus Puurs, 2,26 MWac). The latter project probably has been (co-)financed by world's "most sustainable" bank, the Dutch Triodos Bank (having its roots in the antroposophic movement) via their Triodos Renewables Europe Fund in which the webmaster of Polder PV also has a small participation. The annual report 2010 of this fund claims a "Solar plant Puurs" of 2,3 MWp (apparently DC capacity reported) in its portfolio. Puurs lies just south of the river Schelde, and west of Willebroek, where sustainable bank competitor ASN Bank from the Netherlands co-financed a 2,6 MWp PV-project in conjunction with nuclear power plant co-owner Delta from the same country.

There was also an upgrade of a WDP installation in Boom, adding almost 500 kWac to reach a total capacity of 1.911,4 kWac, while at the same time the long-time mysterious 3,6 MWac entry for Serge Hardy Lanaken (for which not one project detail has been published) has been deleted from the VREG records. It apparently never materialized, pressing further questions concerning the validity of a "VREG-registered" status of (large) PV-installations. Of course, all these tiny, but crucial details have an accumulated impact on the reliability of the PV-market statistics "extracted" from the VREG records (the only "reliable" and verbose dataset publicly available for Flanders).

The most surprising additions to the >1 MWac list however, were two entries for a Zonnecentrale Overpelt NV, 6,20 and 6,22 MWac, that will outstrip the "former ground-mounted champion" Heusden-Zolder system of 4,704 MWac (Flemish province of Limburg) that received its first green certificates on December 19, 2008. The precise location of these two "Overpelt" entries (total app. 12,4 MWac) has not yet been published by VREG, but an internet search revelealed it is built on the premises of metal producer Nyrstar (see photo and info). These 2 biggest entries sofar would have been formally accepted by VREG on December 28, 2010, got their first green certificates on Jan. 14, 2011, and are reported to be connected directly to the ELIA (DNB) power grid (not a surprise given the fact that Nyrstar is a metal producer using huge amounts of electricity). Overpelt is situated in the Flemish province of Limburg alongside the Zuid Willemsvaart canal in a region bordering the southern province Noord Brabant in Netherlands.

The huge Katoen Natie project remains, of course, by far the biggest - roof mounted - installation in the Benelux, see the special further below.

Special: More big players in the Flemish market A number of big players act with large, mostly roof-top PV-installations on the Flemish PV-market. With a lot of money to spend (real estate owners Katoen Natie, WDP), highly professional personnel keen on intelligent roof projects and concepts (e.g., Enfinity), long experience in the installation sector (e.g., SolarAccess, mostly working for big project developers under whose name the project is listed in the VREG records), or good contacts with financial parties, they have realized many large PV-systems in a relatively short period of time. Most of these projects will see very interesting "internal rates of return". Although with politically decided strong degression of feed-in tariffs, in particular for these large projects, the number crackers with these companies will have to redo their homework to be able to realize economically viable superprojects in the near future. Falling module prices and BOS ("balance of system") costs will certainly help to that end, but political support for solar appears to be dwindling due to one-sided "social cost" discussions. At the end of January 2011 I made a selection of some of the most notable big players on the Flemish market, exclusive of Katoen Natie which is considered here as a "very special and unique case" (see special). The source data are published by VREG on a monthly basis in their >10 kWac project listing. In the table, first the main company name (sometimes appearing under a slightly different name), in the second column the number of big PV-projects realised by that company (selection), and in the final column the total capacity involved in these projects (in kWac accumulation). This table adds up to 93 MWp, which represented approximately 14% of total VREG-registered market volume in Flanders, end of January 2011. Mostly projects of hundreds of kWac or even over 1 MWac are included here. The listing is not exhaustive and known newer projects are not yet included.

The table lists a variety of companies, ranging from an energy utility deeply involved in huge amounts of fossil and nuclear power (Electrabel, actually Belgium's super monopolist under major French stake-holder Suez), PV-specialist companies like Enfinity (famous for its fast rise, and active in many countries including China), Belfuture, and Zonnecentrale. But also big retailers like Colruyt and Ikea are highly active, and, as an example of further potential, at a very benign level realizing smaller projects on schools etc., several Flemish communities ("Gemeentes div."). Another "special case" is the bank consortium ING (originating in the Netherlands) that had realised a considerable volume of approximately 5 MWac in 21 projects at that time, mostly via their Equipment Lease branche. GFS Veurne is one of the few "big" free-field installations in Flanders (southwestern part of Belgium, close to the French border). It has been realised by Netherlands (Venlo) based Scheuten Solar together with Flemish project developer Green Fever, and the installation has a size of 2,7 MWp (DC capacity, represented by 2,58 MWac in the VREG records, in two different segments). The "Zonnecentrale" company is also very interesting. Only 6 installations have a total capacity of 10,3 MWac, a spectacular system average of 1.710 kWac per installation. The biggest one is Heusden-Zolder 4,704 MWac (only recently replaced as "the biggest" by a 12,4 MWac project in Overpelt); the other projects can be found in Beringen, Genk, Hasselt, Lommel and Maasmechelen (system sizes between 429 and 2.670 kWac). One of the most striking players shown in this table is, however, a big real property company (in Flemish: "vastgoedbevak"), the stock-exchange-quoted Warehouses De Pauw (WDP). It is represented with almost 11 MWac of large projects in the January 2011 VREG listing, and the company is planning a volume of approximately 30 MW of renewable capacity on or nearby its own warehouses and other property to be able to exploit their business on a "CO2-neutral" basis at the end of "Kyoto" year 2012. In a press release dated April 28, 2010, the company announced it already had 10 MW of PV projects realised in 2007-2009, and that it was planning another 8 MW in a new phase that should end in the first half year of 2011. Already 10 percent of the company's income (5 million Euro/year) is said to originate from the feed-in tariffs earned by these big PV-projects in a news item of August 25, 2010 (and others). Many people in Flanders think that is not the way things should go in Belgium. Because all electricity consumers pay a rate on top of their kWh tariff from which the green certificates are financed by the net managers. Including those for huge projects such as parties like WDP have realised or will build in the near future... |

(b) New installation capacity per month or in the VREG reporting period

An example of a the new capacity per category is given below for the busy month May 2010, in which many new big installations were registered by VREG:

|

© Data:

VREG; Graph: © Peter

J. Segaar/Polder PV, Leiden

(NL) |

This graph shows the newly known capacity that VREG included in their reports, distributed among 7 categories selected by Polder PV. Note that this also included new capacities included for previous years. Due to irregularities in the appearance of the VREG reports, sometimes data of two months are lumped (e.g., March-April), or an incomplete month has been given by VREG (e.g., June, apparently June 29-30 not included). Monthly distributions may vary considerably. In the May 2010 report over 42 MWac of new PV-installation registrations with sizes over 10 kWac were reported by VREG. In February of the same year it was less than 7 MWac. The January 2011 report showed an exceptionally meagre harvest of only 1,4 MWac in this category. Since the periods do not always cover exactly one month, they cannot be simply compared with each other. Therefore, the daily averages for the VREG reporting periods should be calculated, generating a more sound basis for comparison between months. This is presented to you in the next interactive graph, updated up till the end of 2010 (c).

(c) Average new installation capacity per day in the VREG reporting period

This interactive graph shows values calculated from the spreadsheet used for the previous one shown under (b). It reveals big differences in new capacity added to the VREG registrations per month in the period February-December 2010. Since not exactly whole months are covered, the results haven been calculated on a per day basis for each period.

|

© Data:

VREG; Graphs: © Peter

J. Segaar/Polder PV, Leiden

(NL) |

ROLL-OVER IMAGE: Move mouse pointer over the buttonbar below the figure to show the relevant image (status reports by VREG for Flanders in 2010). This graph shows the average of the new installations per day in the given periods only, distributed among 7 categories. Monthly distributions may vary considerably. In 2010, after a sluggish period in March-April, following the end of the "January-February allowance" period for installations not yet having an inverter at the end of December 2009 (decrease of green certificate value from 45 to 35 Eurocents/kWh), May was a busy month again. This is probably the result of delayed registrations by VREG through the time-consuming administrative processes. In the period June 29 till the end of July, in particular the extreme growth of the largest >1 MWac category has been apparent. This is largely to be attributed to the first 9 fragments (total: 15,37 MWac) of the huge Katoen Natie 40 MW project on 4 locations in Flanders finally appearing in the VREG records. Holiday month August showed considerably less activity in the data reported by VREG, and newly registered installation capacities dwindled afterwards. Notably, the collapse of the previous "strong" category of >100-500 kWac installations has been apparent as of October 2010. In November 2010, the >500 up till 1.000 kWac category did not even have one single new registration. The 2 bigger categories were mainly fed by separately registered sub-installations of the huge Katoen Natie project since the summer months, with the addition of only few other big projects not related to the "super" category of Katoen Natie. Further below please find two more graphs visualizing daily average progress for separate categories, extracted by Polder PV from the VREG data.

In the final graph of this section the per day graph for the last month reviewed by VREG is shown, revealing the data for Feb. 28 up till April 5, 2011 (36 days):

|

© Data:

VREG; Graph: © Peter

J. Segaar/Polder PV, Leiden

(NL) |

For interactive graphs under (c) legend: grid connected systems > 10 kWac only; light green = number of new registrations (left Y-axis); light orange = new added capacity (MWac or kWac) in the period under consideration, per category. Graph (b) shows the total capacity and/or number of registrations in the given example. Graph (c) gives the capacity and/or number of installations per day and per period (interactive) as extracted and calculated from the data reported by VREG.

For the reported multisite project Katoen Natie 40 MW on 4 locations in Flanders, parts of which for the first time were incorporated into the VREG statistics in the July 2010 update, new portions were added in the later updates, starting with August 2010. This huge project (cost: € 166 million), partly financed by loans from Dexia Bank and another, unnamed bank, is cut into a lot of smaller pieces between 0,21 and, possibly, 2,22 MWac under various (new) company names. Most probably for financial reasons (optimal taxation issues related to the green certificates earned?). Up till the October update, only one installation was mentioned under the identifiable name "Katoen Natie Terminals NV", a second segment under that name followed in the November update, but all the other projects have been filed under different sub-company names (and in a later stadium designated as such by VREG in their installation records).

Two new entries appeared in the Jan. 1, 2011 update, under the location Sint-Kruis-Winkel (together 3,27 MWac), for Katoen Natie daughters Polymer NV and Sabeen NV. These are at the same installation location address for which already a "Desteldonk" entry was known, accumulating to 4,95 MWac for these 3 subprojects in the sea harbour region of northern Gent. In addition, a fourth entry was filed under the name Seaport Terminals NV (1,485 MWac) on that date, with Sint-Kruis-Winkel as location, and a fifth entry under the same name and with identical size in the Feb. 28, 2011 report, again with Desteldonk as location (all: same zip-code and same address...). The latter two are on exactly the same address, on different logistics halls (numbers 17-19 and 19-21; the three Katoen Natie entries here have been realized on halls 14-16, 26-30 and 36-39), but it could not yet be established if Seaport Terminals N.V. is a daughter company of Katoen Natie or not (VREG does not give a positive clue in this direction). As for now, the Seaport Terminals entries are not considered as part of the "Katoen Natie" super project.

Also note that one of the smaller (246,3 kWac) "Kallo (Kieldrecht)" segments has been earmarked with an address that is on the eastern side of the Vrasene Dock, more to the southwest of the Loghidden City complex (Land van Waaslaan Haven 1168/Saeftinghe Loods 5). So actually this is a separate location. Still no "hits" appear to have been included for the so-called Euroterminal of Katoen Natie to the southwest of that separate Vrasene Dock, that has been said to be part of the whole 40 MW project.

The April 5, 2011 VREG report lists 22 portions (27,51 MWac) for the Kallo-Kieldrecht location on the Schelde West-Bank (not on Antwerp soil, but nearby on the premises of the province of East-Flanders). In addition to this, now at least 5 portions for the Katoen Natie logistics terminal in the Desteldonk/Sint-Kruis-Winkel area are known in the harbour region northeast of Gent (also on soil of East Flanders; 8,12 MWac). Finally, 2 installations in the Katoen Natie terminal area of Genk in the Flemish province of Limburg in the northeastern part of Belgium are also reported with a total size of 2,15 MWac under the prozaic (and confusing) company name "Ghendt Handling And Distribution NV" (which has its main office in Desteldonk/Gent...). Taken all together a total capacity of 37,8 MWac for the multisite Katoen Natie project has now been registered with VREG and positively identified as such to that project. Note that this volume still is only 94,5% of the total of 40 MW announced as early as end of 2009. But it is also possible, that the frequently mentioned "40 MW" may be the DC power of the whole project, which could easily match 37,8 MW of max. AC power of the inverter systems involved.

From the data so far extracted from the VREG records, it is crystal clear that the Kallo-Kieldrecht location, named "Loghidden City" by Katoen Natie has, with its 22 portions now registered by VREG, 27,51 MWac. Since the VREG report for July 2010 it already is officially the largest realized "single site" PV (but multi-roof) project in the Benelux, with decreasing possibility that more volume will be added in coming VREG reports. As of now, the actual status of the other portions of this enormous roof PV-project remains enigmatic as well. Euroterminal, also in the West-Bank area of Antwerp's huge harbour region extending into East-Flanders, has not been specifically mentioned yet by VREG.

Not

belonging to "Katoen Natie"? Sofar, no distinct connection of this company (G.W.S.) has been found in relation to the Katoen Natie holding, despite the fact that several K.N. entries have a somewhat reminiscent daughter company name ("Ghendt Handling And Distribution NV", 2 of them in Genk, and one single site just southwest of Katoen Natie's "Loghidden City" on the Schelde West-Bank). Activities of both companies clearly are focussed on large-scale warehousing services - in exactly the same harbour areas. Together these 4 Desteldonk Ghendt Warehousing sub-projects accumulate to an installation size of 1,352 MWac. |

Katoen Natie line-up

One of the interesting new data since publication of the Jan. 31, 2011 Excel spreadsheet on the VREG website is the fact that per installation the official installation date is show, as well as the date on which the first green certificates have been awarded to the project (actually the final step in the whole "official procedure" for PV with the VREG administration). With these data it could be shown that for the now 29 positively identied installations for the Katoen Natie super project a time span of less than 4 months lapsed between the official installation dates for the first (Sep. 4, 2009), and the last sections identified (8 sections on Dec. 31, 2009). But that over 14 months have lapsed between the dates on which the first green certificates issued for the first (Sep. 3, 2009) and final two sections (November 16, 2010) incorporated in the April 5, 2011 VREG update. I summarised the findings in the following 2 new graphs.

|

^^^ See next graph for the dates on which first green certificates were issued for the separate sub-installations of Katoen Natie by VREG. |

|

^^^ Indicated in numbers are either the capacities of single sub-projects per issue date, or the accumulation of the capacities if different sub-projects were issued on the same date (per location). If more than one sub-project is shown in one column, the number of sub-projects for that column is shown in brackets. The total of sub-projects positively identified as belonging to Katoen Natie amounted to 29, 22 of them for Loghidden City (actually one small sub-project lying very close, for now included in the Loghidden City data). Total capacities identified for the three main locations are indicated in the legend. The red line indicates the start of the new incentive scheme beyond the "transition period" allowed by the Flemish authorities. If installations had the modules in place end of December 2009 (with report of preliminary approval), and were able to have the PV-system completed with inverters end of February 2010, they would be eligible for 45 Eurocents/kWh feed-in tariff for 20 years. If that dead-line had not been realized in time, the installation will only fetch 35 Eurocents/kWh for 20 years (if installed completely in 2010). Also all other installations not having the modules in place end of 2009, and newly realized in 2010, will get that much lower (but still highly interesting) premium. As per January 2011 new degressions have been decided, starting with 33 Eurocent/kWh on that date (no transition period). These considerations do not apply to the Katoen Natie project, since all sub-installations apparently have passed the "transition period" without problems, and can apply for 45 Eurocent/kWh for 20 years. Note that the time-scale in this graph is different from that used in the previous graph for the "Date of official installation". |

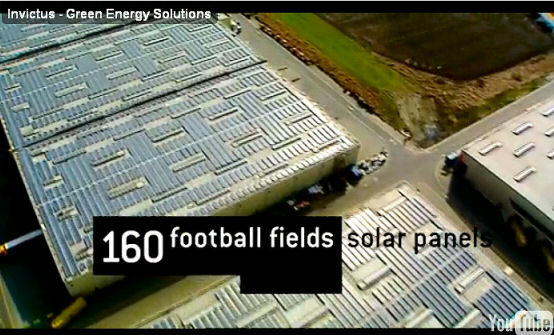

Five installations under the same "Katoen Natie umbrella" have been registered as such in the Desteldonk/Sint-Kruis-Winkel/Gent region (Mai Zetterlingstraat 70, see photo of the complex on the Katoen Natie website), as well as two on the Katoen Natie logistics terminal in the industrial area south of Genk in the Flemish province of Limburg. On the latter complex, 2,15 MWac has been registered in 2 segments for the company Ghendt Handling and Distribution N.V. This website shows that this company also is part of the large Katoen Natie holding. Overall, still a few MW of the multi-site superproject might not yet been validated (or approved, or fully registered) by VREG. The 40 MW project was "claimed" as such at the end of 2009 by the principles of Katoen Natie in a few short press communications and television broadcasts. It still is not clear if the "40 MW" claimed refers to AC capacity, or possibly to the MWp nominal capacity of the PV-modules involved (source: Trina Solar, China). See also the photograph below.

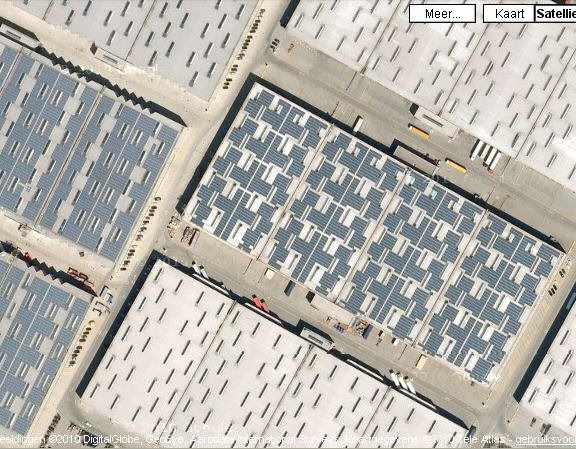

Photo © 2010

DigitalGlobe, Geo Eye, Aerodata International Surveys / Google

Maps project (this

location).

Photo 1 - The first Katoen Natie terminal buildings filled with Trina Solar modules were appearing in Google Maps satellite photo's midway 2010, such as this one. Three halls had been completed already at the time that this photo was taken. It shows the southwestern part of the huge "Loghidden City" complex in the Kallo/Kieldrecht harbour region northwest of Antwerp on East-Flanders province soil (Schelde West Bank). Other halls appeared to have already mounting frames in some areas, but most halls did not show any roof-related activity yet. However, a company video by installer Invictus shows that at least this "Loghidden City" complex is mostly filled with crystalline PV-modules - although a small volume of the reported multi-site 40 MW project still might not be documented in the VREG statistics (status: April 5, 2011 update).

Note the lorries on the photo to get an impression of the enormous scale of this logistics complex. It is also evident from the satellite pictures that the halls, and also the modules themselves are oriented in arrays slightly south from SW. This has only slight impact on physical production, not deviating much from a pure south orientation. The project as a whole (at least three different locations) should produce in the order of 35 GWh/year according to press releases. This could indicate an expected specific production of only 875 kWh/kWac.year. This might be a conservative estimate.

The first partial projects of this site ("Kallo/Kieldrecht" location) have been reported by VREG in the August 1, 2010 report (8 segments on this location and one in Gent/Desteldonk, total of these: 15,37 MWac); more sections followed in later VREG reports.

Flanders:

distribution among PV-installations < 10 kWac

Installaties kleiner of gelijk dan 10 kWac in Vlaanderen: verdeling

Once the number and capacity of the accumulated > 10 kWac installations is known from the separate list for that category (previous paragraph), it is easy to obtain the data for the smaller PV-systems in Flanders since VREG also publishes a list ("Productie-installaties waarvoor groenestroomcertificaten worden toegekend") with accumulations of the capacities and numbers for all renewable electricity generating installations. By subtracting the volumes for the > 10 kWac category PV-systems from the accumulation given in that list for all (PV-)installations, the data for the remaining < 10 kWac installations can be calculated. This results in the two following graphs. First total volumes and their distribution are shown for photovoltaics.

Relative

contributions of market segments in photovoltaics Flanders

In this graph

in the left "100 percent column" the share of the categories

discriminated by me

(all

installations

up till

10

kWac,

and 7 subcategories

larger than 10 kWac) is shown for the numbers of installations (for

the largest systems sometimes separate entries of fragments, such as

Katoen Natie's Loghidden City: one complex, 22 entries). From that

column it is crystal clear that the <10 kWac segment of the

market

is the unparallelled contributor, with 98,4% of all PV-installations

(or segments) installed.

A very different outcome shows up when the installed capacity is taken as the discriminating value, as depicted in the right "100 percent column" with stacked categories ("MWac"). Here, the <10 kWac segment only claims 58,5% of accumulated installed (AC) capacity, and over 40% is claimed by installations each having a capacity larger than 10 kWac. Of those, the biggest "total capacity contributor" is the >100 up till 500 kWac segment with 15,3% of accumulated photovoltaic AC capacity. The "top" market segment, installations (or system segments) larger than 1 MWac each, claim 12,8% of total accumulation, and the >500 up till 1.000 kWac segment contributes 7,0%. The contribution of the market segments >10 up till 100 kWac is much smaller to negligible.

Note that VREG does not further discriminate any subcategories in the "small" market segment up till 10 kWac. Hence, no further "split" can be made in the white column parts in this graph.

Relative

contributions of PV-systems in the >10 kWac category

In

the largest market segment >10 kWac, I also distinguish between subcategories,

and the contribution of those in the installated volume for only that market

segement (hence: not for all PV-installations) has been visualized in the

next graph.

The same scheme is applied here as in the previous graph. For "100 percent" now the accumulated volume for only the >10 kWac market segment is used (number of installations and inverter capacity, respectively).

In the left column, shares of the 7 subcategories discriminated by me have been shown with respect to the number of installations (or installation segments separately registered by VREG), revealing dominance of the >100 up till 500 kWac subcategory (30,5%). Shares are relatively well spread among subcategories, however with minor contributions of the >10-15 kWac, and the 2 largest subcategories.

In the right column, again accumulated capacity (MWac) for each subcategory is the discriminating feature in relation to accumulated installed capacity for the >10 kWac market segment. Here, again the same >100-500 kWac subcategory leads the way (share of 36,9%), followed by the two other important top subcategories, larger than 1 MWac (30,8%), and >500-1.000 kWac (16,8%). These top 3 subcategories together make up 84,5% of total installed/registered capacity in the >10 kWac market segment. For comparison, please note that installations >100 kWp were not allowed under the highly restrictive SDE "incentive" regime in the bordering Netherlands up till 2010.

Average of new installations per day

The listings for all new PV-installations (accumulation of numbers and nominal capacity only), and the one for the individual >10 kWac PV-systems are published separately by VREG. The publication date of these updates can differ slightly. To be able to compare the progress in new installations on a daily basis for the category larger than 10 kWac as well as that for the smaller PV-systems (max. 10 kWac), separate calculations have been carried out by Polder PV for the average daily newly reported capacity, as well as for that of the >10 kWac systems. Average daily progress in new VREG registrations has been calculated by dividing the growth in the monthly report under consideration by the exact number of days spanned by that report. Furthermore, to obtain the daily average for the <10 kWac pool, the calculated values were subtracted (total average minus average for >10 kWac group). With the results, I could obtain the following graphs, showing the considerable fluctuation in daily average level of registration on a monthly basis for both groups considered.

^^^

Stacked

graph

Results

for both groups stacked to show average daily progress in the periods

designated on the X-axis. Note that these need not represent exact

monthly periods. For example, there were no separate reports for March

and April 2010, so the average daily growth for both months together

has been calculated. Not all months were fully covered in one report. Therefore,

the result

for that month has been calculated from the span within that month

as indicated by the dates of publication indicated by VREG. Examples

are June (1-29) and October (1-28) 2010. Note

that the daily average for new registrations in the category >10 kWac

installations (green column

segments in this graph) fluctuates considerably through the months

of the year, in between 247 and 1.651 kWac on average per day up till

2010 (difference maximum factor 7). Which can be attributed only partly

by the inclusion of very

large installations > 1 MWac in a certain period. An "all-time-low" is

apparent in the VREG registrations for January 2011, only 47 kWac added

per day in that month for the "big" category. It

is expected that long validation and registration times might also

play

an important

role in the uneven distribution of these large installations in the

VREG registration statistics. For example, the 40 MW Katoen Natie

project, already reported as "installed" end of 2009, still

might not have been fully

registered

as

of

April 5,

2011, in these statistics (still a few MW missing).

Another example: The 1,87 MWp amorphous silicon thin-film project on the Flanders Expo, already reported by me begin of December 2009, only has reached the VREG listing in the April 5, 2011 report (in 5 separate entries with 1,596 MWac, hence DC/AC ratio of 1,17), thus showing the long time between project realisation and VREG registration.

The smaller market segment of <10 kWac (blue column segments in this graph) shows a more stable development, ranging between 316 in the Spring months March/April up to a notable end-of-year mini-rush of 816 kWac in December, average per day (factor 2,6 difference). For all installations together, July was a real record breaker, new installations being recorded by VREG with an average of 2.133 kWac a day. Note that, while January 2011 has been a dramatic month for development of the market registration for installations > 10 kWac, the registrations for smaller PV-systems appeared to be unaffected, with a healthy 482 kWac/day of new installations. February and March 2011 continued that healthy trend with almost 600 kWac a day.

Graph

aligned + trends

In the

next graph the results for both market segments are shown alongside

each other:

For both categories also (Excel-generated) linear trend lines have been incorporated in the graph. For the period shown (February 2010 up till March 2011), there is a conspicuous downgoing trend for the daily average new capacity registered for installations > 10 kWac by VREG (green dashed trend line). Instead, a clear upward trend is apparent for the PV-systems with a maximum size of 10 kWac in the VREG registrations (blue dashed trend line). One should be cautious to interpret these as "real market trends". Predictions as to how the two market segments will evolve are hard to make, and will be highly effected by the degression steps in the feed-in categories decided upon by the Flemish authorities (see interactive graph with the degressions to be implemented in coming years, analyzed by Polder PV on December 11, 2010). Another critical factor will be the "perception" with the Flemish inhabitants, as publications related to solar development, costs, and benefits, appear more frequently in the newspapers, magazines, radio, TV and, of course, on the internet. Finally, the delay in registration in the VREG records, sometimes long after installations have been connected to the grid is a factor making interpretations of market development in Flanders a difficult task.

Detailed

graph for segment > 10 kWac

For

the market segment of >10 kWac installations, for which individual

system size details are available in a long list on the VREG website,

a more

detailed daily average graph could be made:

Detailed split of the 7 capacity categories discerned by Polder PV to show development in average daily new registrations in the periods shown on the X-axis (month reports by VREG). In particular the larger categories >100 kWac fluctuate considerably in the course of time. If this is "true installation reality", or that it might be a flaw of the administrative delays in the registration system with VREG, or perhaps both, remains unclear. The peak in the period June 29 up till August 1 ("July") for the largest category >1 MWac (green curve) could be attributed to the first 9 sub-installations of the Katoen Natie superproject being registered by VREG, resulting in a "month-average" of 792 kWac newly installed capacity for that category per day.

Note that in the Dec. 1, 2010 report, an installation of 12 kWac in the small market segment of installations up till 15 kWac has been removed in the VREG update, which resulted in a slight "negative growth" for the last month in this graph (not discernable at this detail level). In the April 5, 2011 report 7 smaller installations in the >10 kWac category (10-15 kWac), and the 3,6 MWac Serge Hardy project have been removed for unknown reasons. Sometimes upgrades (capacity) and renewals of previously registered installations occur in several VREG month reports, but in general they have only minor influence on general "growth" trends such as depicted in the graphs in this section.

The graph shows very clearly the considerable negative impact on the registered market growth in all segments > 10 kWac at the start of the new year (2011). Growth in registrations had almost come to a stand-still in January 2011. Luckily, February and March 2011 showed a positive development again.

Calculation

of the impact of the market segment of maximum 10 kWac

When subtracting the capacity of 310,31 MWac for the > 10 kWac

installations (graphs above) from the reported total of 747,29 MWac in

the separate installation

listing in the VREG April 5, 2011 update, a volume of 436,98 MWac remains

for the "maximum 10 kWac" installations market segment.

With installations removed from the most recent VREG list taken into account, the number of installations > 10 kWac turned out to have grown to 1.589 in the April 5, 2011 report (average size for that category: 195,3 kWac/installation). VREG reported in the same month a total accumulation of 100.935 registered PV-installations (report also date-stamped April 5, 2011). Hence, 99.346 systems (or, preferrably: "registrations") should be allocated to the category of max. 10 kWac installations.